1

1Financial Markets Conduct Act 2013: Wholesale Investor Exclusion under the Disclosure Regime

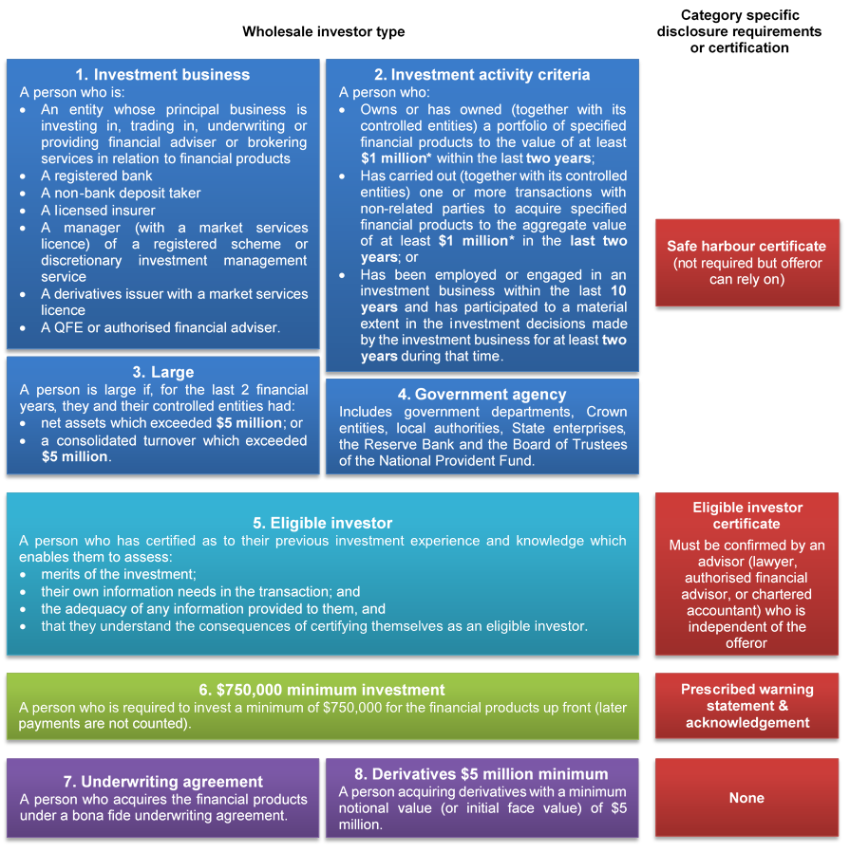

Set out below is an overview of the FMCA “wholesale investor” exclusion that permits issues to investors that are considered able to look after themselves. It is important to note that even if an offer is made in reliance on an exclusion, the FMCA may still impose short-form disclosure, warning statements or other requirements on the offeror. Please click here to see further information about the FMCA disclosure requirements and other FMCA disclosure exclusions. Wholesale investor exclusionDisclosure under the FMCA is not required if the investor is what is known as a “wholesale investor”. There are eight categories of “wholesale investor”: 1. investment business;

2. investment activity criteria;

3. large;

4. government agency;

5. eligible investor;

6. $750,000 minimum investment;

7. underwriting agreement;

8. derivatives $5 million minimum.

How do I know if the person is a 'wholesale investor'?Categories 1 to 5: These exclusions are not straight forward as they depend on the nature of the investor and the offeror may not have these details. Helpfully, an offeror can rely on a prescribed certificate from an investor to confirm that the investor is a wholesale investor under these categories:

Safe harbour and eligible investor certificates are valid for two years unless revoked earlier by the investor. Categories 6 to 8: These exclusions depend on the nature of the offer so offerors can more easily assess for themselves whether these exclusions will apply. Remaining obligationsOfferors who rely on a wholesale investor exclusion will still need to be aware of the following FMCA obligations:

Wholesale investor summary chart

* The value of a derivative is treated as the face value on entry divided by 10. The term financial products in the FMCA is very broad and covers debt, equity, managed investment products and derivatives. Disclaimer: This article is a general summary of complex laws and regulations that contain severe sanctions for breach and is not intended as legal advice. Specific legal advice should be obtained in relation to proposed marketing, offering or selling of financial products. All rights reserved © Jackson Russell 2017 |

Contact Darryl King, PARTNER |